Most retail traders open their first forex broker account in the first six months of their journey and stay there out of inertia rather than because it remains the best fit. Spreads creep up without notice, withdrawal speeds slow, regulation shifts, or a competitor launches tighter pricing. This guide walks through how to switch forex brokers without losing money, blowing up open positions, or getting stuck in a withdrawal limbo. CFD trading involves significant risk and 74–89% of retail investor accounts lose money. This content is informational and does not constitute financial advice.

Written By

ForexRater Editorial Team

Data-driven broker comparison · Independently tested · No paid rankings

Reviews represent the editorial opinion of ForexRater and are not personal financial advice.

Why Traders Switch Brokers — And When It's the Right Move

Industry data from regulator complaint logs and broker churn studies suggests the average retail trader changes broker roughly 2.3 times in their first five years. The trigger is rarely a single dramatic event — it's usually a quiet accumulation of small frustrations that eventually outweigh the friction of switching.

The most common reasons traders give for changing forex broker are: spreads have widened without an announcement, withdrawals are taking longer than they used to, the platform freezes or disconnects during high-impact news, the broker has lost or downgraded its regulatory licence, a competitor offers materially lower commissions for the same execution quality, or customer support has become slow and scripted. Any one of these in isolation may not justify a move. Two or three together almost always do.

It is also worth being honest about when switching is the wrong move. If you are switching because you lost money on a trade and want to blame the broker, the next broker will look identical inside three weeks. If you are switching purely chasing a deposit bonus, you will likely surrender more in trading costs over the bonus turnover period than the bonus is worth. And if you are switching because of a single platform outage during NFP, check the broker's status page first — every broker has had at least one bad print day, and reputable ones publish post-mortems.

The right time to change forex broker is when you have measured your actual trading costs over a full month, compared them to two or three regulated alternatives, and found a structural saving — not a marketing one — that justifies the operational overhead of the move.

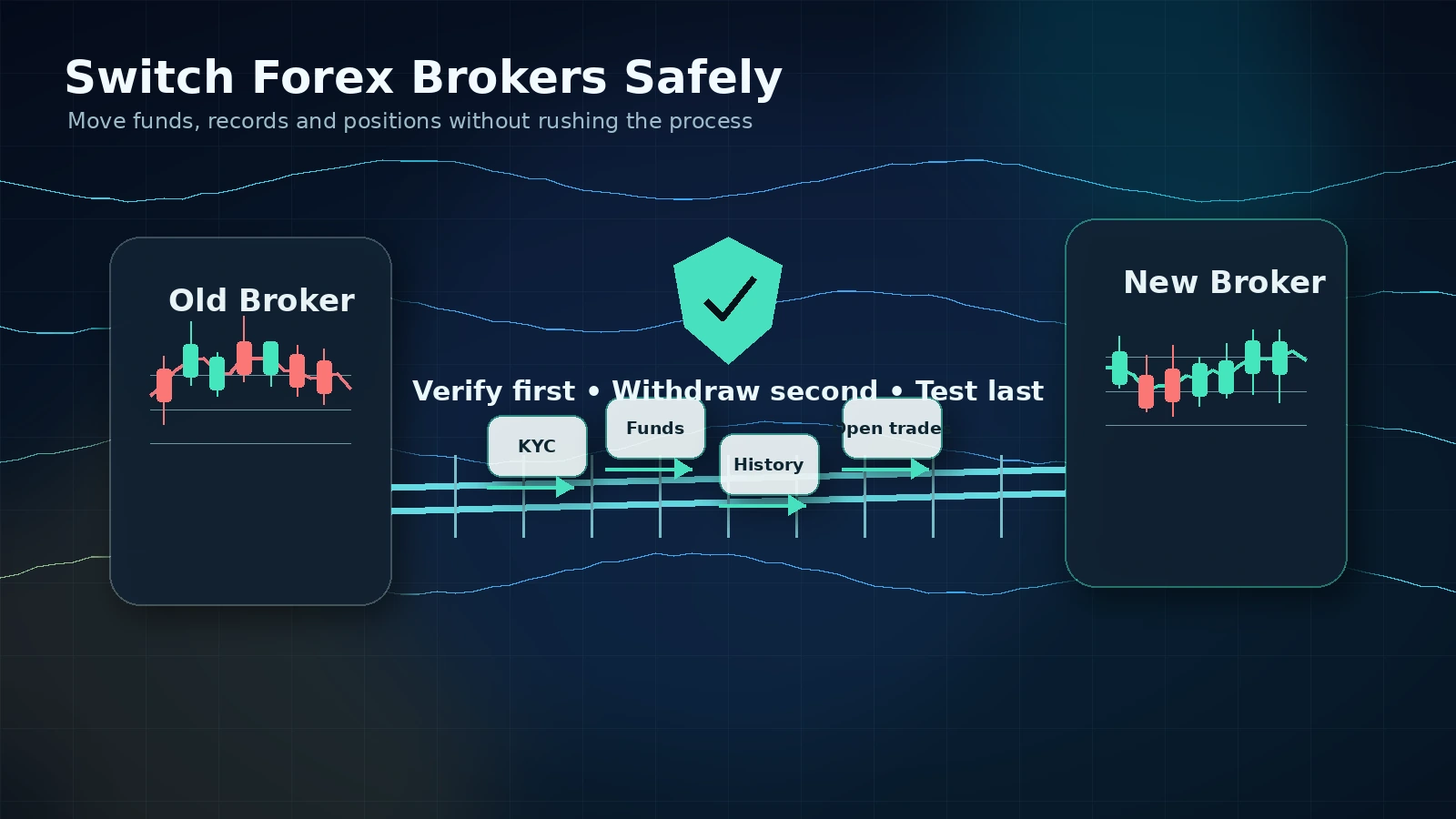

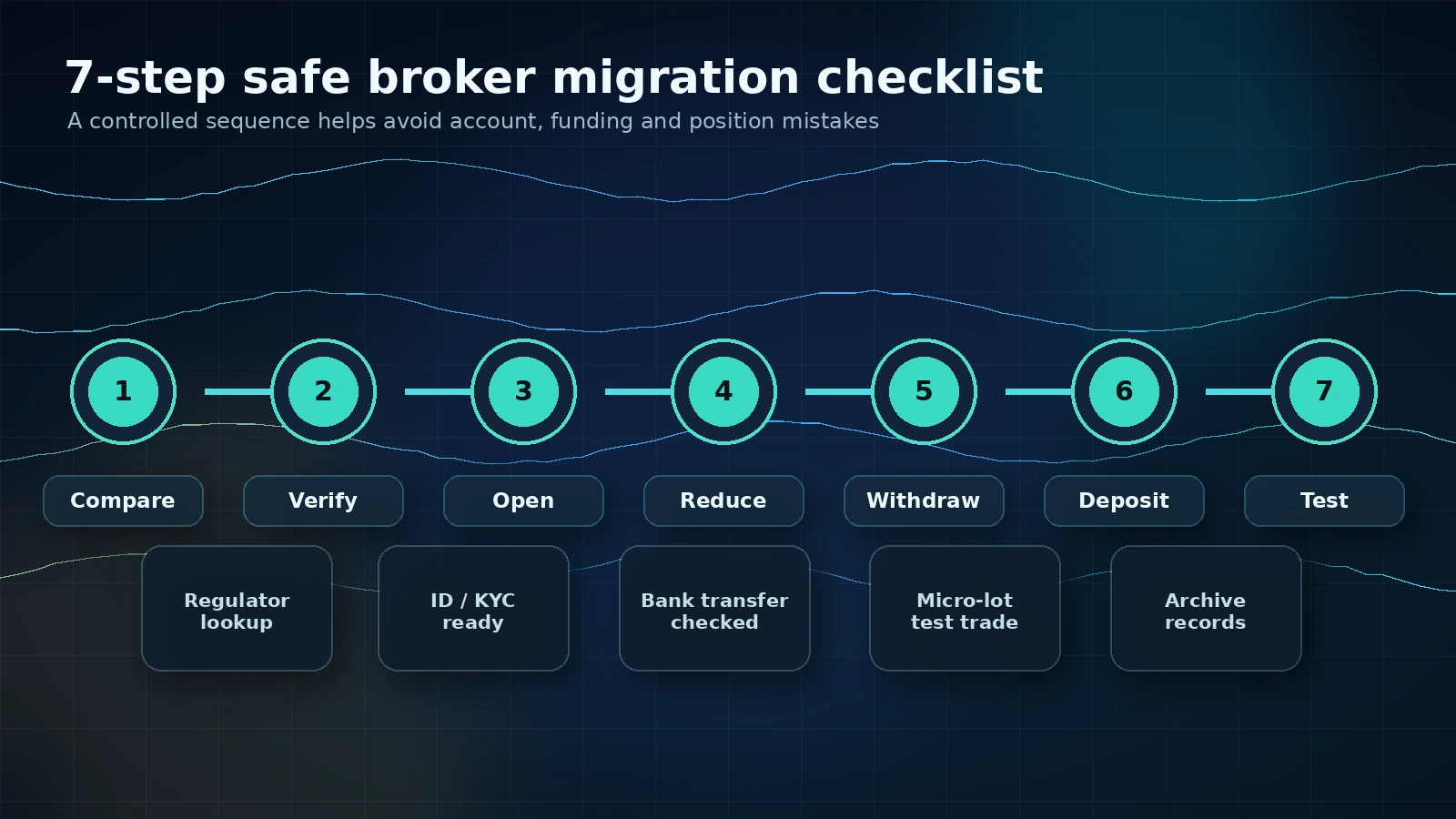

The 7-Step Process for Switching Brokers Without Losing Money

The single biggest mistake traders make when switching forex brokers is closing the old account before the new one is funded and tested. That leaves you out of the market — and if the move was triggered by deteriorating spreads, you have effectively guaranteed the worst possible execution on your remaining trades. Follow this order instead.

1. Choose your new broker first. Build a shortlist of two or three regulated alternatives and compare them on the specific instruments you actually trade, not the marquee pairs. EUR/USD spreads are a poor proxy for what you will pay on AUD/JPY or gold.

2. Verify regulation independently. Do not trust a broker's website. Search the firm's name directly on the FCA Register, ASIC Connect, or MAS Financial Institutions Directory. If the entity you are about to deposit with is not the one listed, walk away.

3. Open and verify the new account. ID and proof-of-address verification typically takes 24–48 hours at Tier-1 regulated brokers. Get this done before you touch the old account.

4. Close or reduce open positions strategically. Never close everything at once. Phase out over several sessions to reduce the chance of being caught the wrong way during the transition. More on this in the next section.

5. Request the withdrawal. Withdraw to the same funding method you deposited with — anti-money-laundering rules require this and using a different method is the most common cause of withdrawal delays.

6. Deposit into the new broker. Match the funding method again. E-wallets clear in hours; bank wires take 1–3 working days for Tier-1 regulated brokers.

7. Test with a small live trade before committing. One micro lot on a major pair tells you more about real spreads, slippage, and execution than a week of demo testing on the same platform.

| Broker Type | Bank Transfer | E-Wallet | Card |

|---|---|---|---|

| FCA / ASIC Tier-1 | 1–3 business days | Same day – 24 hours | 1–2 business days |

| CySEC / MAS | 2–5 business days | 24–48 hours | 2–3 business days |

| Offshore / Unregulated | 5–14 days (often longer) | 2–7 days | Variable |

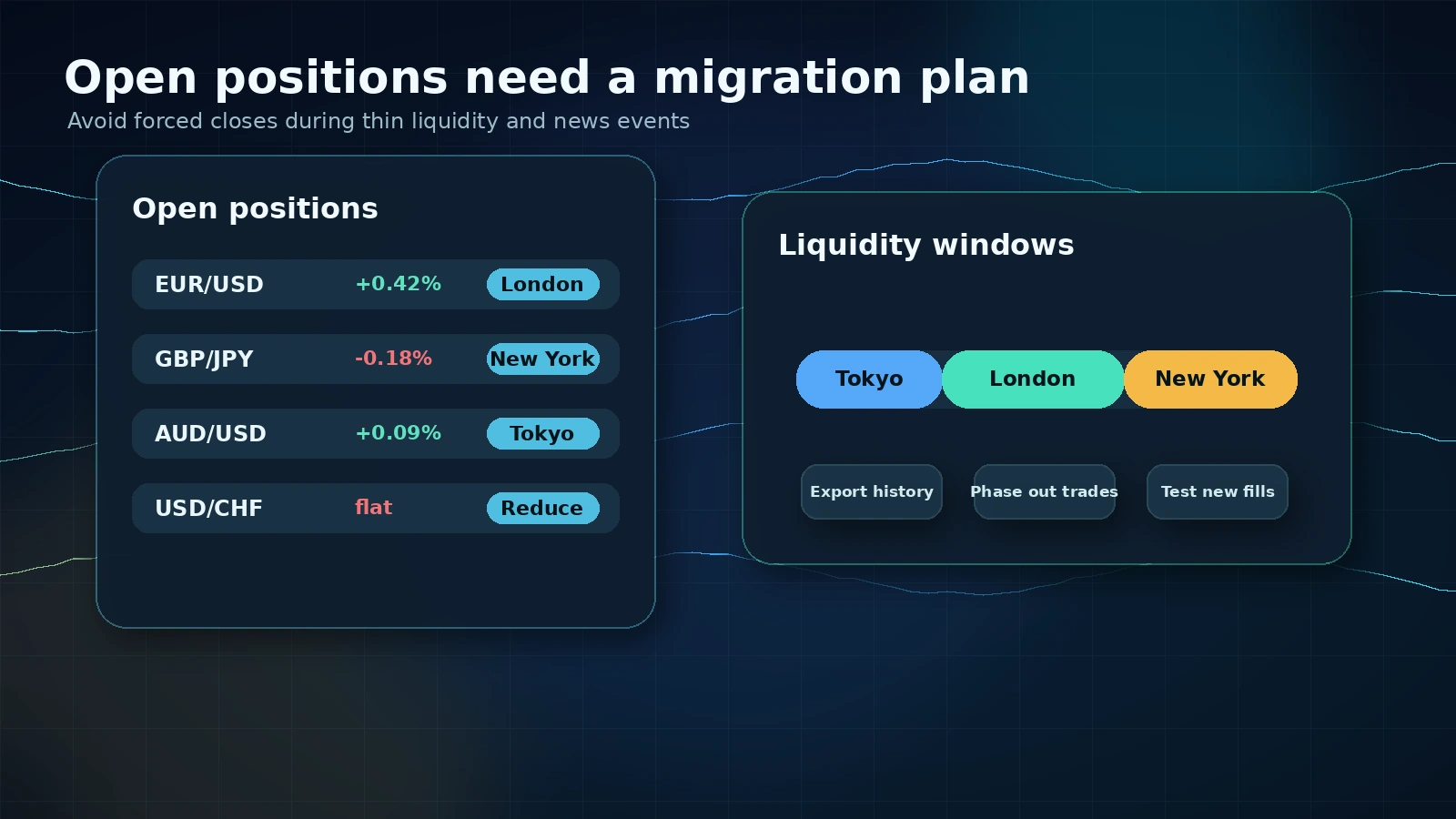

What to Do With Open Positions When Switching

Open positions are the part of switching that costs traders money when it goes wrong. The temptation is to flatten everything in one click and start fresh — but that means accepting whatever spread and slippage are on offer at that moment, which is rarely the best price you will see that week.

The cleaner approach is to phase out over several sessions. Close the largest and most spread-sensitive positions first during the most liquid window for that instrument — London open for EUR-crosses, the London/New York overlap for the majors, the Tokyo session for JPY-crosses. Leave smaller and less time-sensitive positions until last so that you are not forced into thin liquidity.

If you carry positions with strong negative swap — short JPY pairs at the moment is a familiar example — and the new broker offers materially better overnight rates, the swap saving alone can pay for any spread cost on the transfer. Calculate this before you decide which positions to close versus which to re-open at the new broker.

Some traders hedge during the transition by opening an offsetting position at the new broker rather than closing at the old one. This neutralises directional risk while funds are being moved, but it doubles your margin requirement and you are paying spreads on both sides — only worth it for large positions where directional exposure during the move is a real concern.

Before you close the old account, export your complete trading history. In MetaTrader 4 and 5, right-click in the Account History tab and choose Save as Detailed Report. Save the HTML and a CSV copy. Take screenshots of equity, balance, and any open positions. You will need these for tax reporting and, in the unlikely event of a dispute, as evidence of what was on the account when you left.

Withdrawal Red Flags — Signs Your Broker Is Stalling

A regulated broker withdrawing in three working days is normal. A broker manufacturing reasons to delay your money is one of the clearest signals that you should never have funded the account in the first place. Five red flags appear again and again in regulator complaint files.

The verification loop. You upload ID. They request proof of address. You upload it. They request a clearer copy. You send it. They request a utility bill instead of the bank statement you sent. This is a tactic, not a process — Tier-1 regulated brokers complete verification once.

The fee that wasn't in the original terms. A withdrawal fee, conversion fee, or processing fee that appears at the moment of withdrawal but was not disclosed at deposit is a breach of consumer regulation in every Tier-1 jurisdiction. Document the deposit terms and the withdrawal terms side by side, then complain to the regulator.

The bonus clawback. If you accepted a deposit bonus, the small print almost always requires you to trade a multiple of the bonus before withdrawing. Some brokers go further and claw back not just the bonus but any profit derived from it — leaving you withdrawing less than you deposited. Read the bonus terms before accepting; better still, refuse the bonus.

The compliance review. Your withdrawal is paused for "routine compliance review" with no timeline. Legitimate compliance holds are rare and time-bound. Open-ended holds are a delay tactic.

The recurring payment processor issue. Your first withdrawal request fails because of an issue with the payment processor. The second also fails. The third gets blamed on the bank. Tier-1 regulated brokers do not have rolling payment processor problems — they have multiple redundant providers.

| Indicator | Tier-1 Regulated | Offshore / Unregulated |

|---|---|---|

| First withdrawal time | 1–3 business days | 5–30+ days |

| Verification rounds | 1 | 3+ (often unlimited) |

| Recourse if stalled | Regulator + ombudsman | None practically available |

| Hidden fees | Disclosed in fee schedule | Frequent and changing |

Best Brokers to Switch To in 2026

The brokers below are the four we see most often as destination accounts in our reader survey data. All four are Tier-1 regulated, all four are ECN/STP execution, and all four publish their pricing transparently. Independent comparison only — do your own due diligence against your own jurisdiction's rules.

IC Markets — ASIC, CySEC and FSA regulated. Raw spreads from 0.0 pips on EUR/USD with $3.50 per side commission ($7 round-turn). Some of the deepest liquidity available to retail clients and consistently strong execution data on third-party tests. Best fit for active scalpers and EA traders. Visit IC Markets

Fusion Markets — ASIC regulated. Among the lowest-cost ECN options for retail clients — $4.50 round-turn commission and raw spreads. Smaller and newer than IC Markets but the cost structure is industry-leading on the major pairs. Best fit for cost-sensitive day traders. Visit Fusion Markets

Vantage — ASIC, FCA and VFSC regulated. Stronger on copy trading via the Vantage Copy platform and more polished mobile app than the pure ECN names. Slightly higher commissions than IC Markets but a wider product mix including indices and commodities. Visit Vantage

VT Markets — ASIC and FSCA regulated. Solid mid-tier alternative if you want ECN-style pricing without the largest brokers' minimum activity expectations. Read our full VT Markets review for the detail.

Whatever you switch to, give the new account a 30-day shakedown period with reduced size before you commit your full account equity. Run the same strategy you used at the old broker on the same instruments and compare your actual fill quality. That is the only test that matters.

Risk warning. CFD trading involves significant risk and 74–89% of retail investor accounts lose money trading CFDs with the providers listed. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. This article is informational and does not constitute financial advice.

📖 Key Terms — Forex Glossary

Not sure about a term?Browse our full Forex Glossary →

Frequently Asked Questions

Expert Answers to Common Queries