Forex brokers are not charities and they are not running their platforms for free. Understanding exactly how your broker makes money tells you whether their incentives are aligned with yours, where the hidden costs sit, and which broker model suits your style of trading. This guide breaks down the three revenue streams every broker uses, the difference between A-book and B-book execution, and the practical signs that your broker may be on the other side of your trades. CFD trading involves significant risk and 74–89% of retail investor accounts lose money. This content is informational and does not constitute financial advice.

Written By

ForexRater Editorial Team

Data-driven broker comparison · Independently tested · No paid rankings

Reviews represent the editorial opinion of ForexRater and are not personal financial advice.

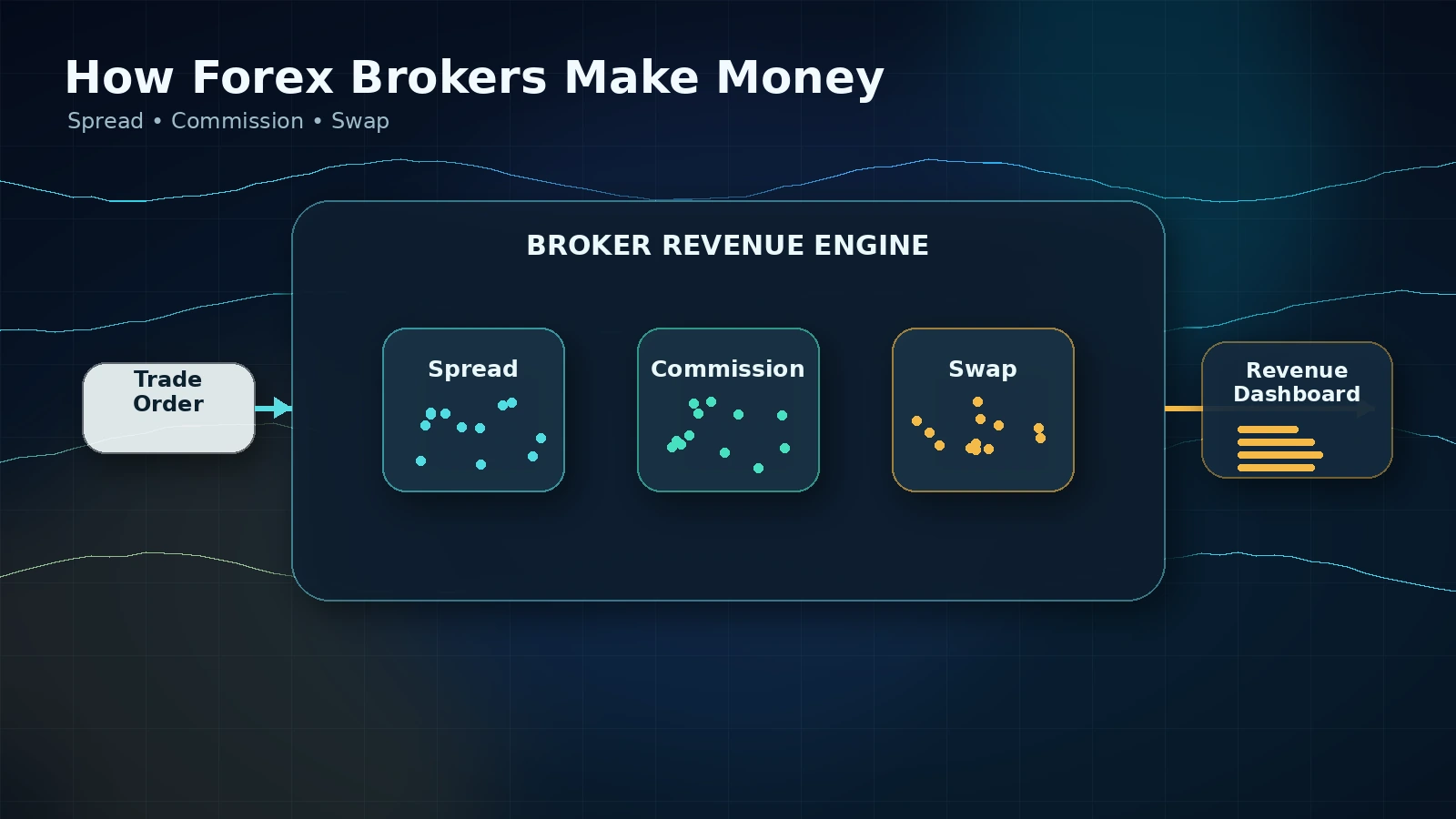

The Three Revenue Streams Every Broker Uses

Every retail forex broker — without exception — earns from some combination of three sources: the spread, the commission, and the overnight swap fee. The mix differs sharply between brokers, and it is the mix that tells you what type of broker you are dealing with.

The spread is the difference between the price at which you can buy a currency pair and the price at which you can sell it at that same moment. If EUR/USD is quoted 1.08501 / 1.08507, you pay 0.6 pips to enter and exit. On a single standard lot (100,000 units of the base currency), a 0.6-pip spread on EUR/USD costs you roughly $6. Across a broker handling $100 million of daily client volume on that single pair, even a fraction of a pip captured on every trade compounds into substantial revenue.

Commissions are explicit per-trade fees charged on ECN-style accounts that offer raw (near-zero) spreads. Typical retail commissions are $3.50 per side per standard lot — $7 per round-turn. The trade-off is straightforward: tighter spread plus a commission almost always beats a wider all-in spread for active traders, but the maths only tilts that way above a certain volume.

Overnight swap fees are the interest paid or received for holding a position past 5pm New York time. The size and direction of the swap depend on the interest rate differential between the two currencies in the pair and on the broker's own funding markup. Long EUR/USD has been a negative swap trade for most of the past decade because EUR rates were below USD rates; long USD/JPY has been a positive carry trade for the same reason in reverse.

A broker offering you 0.0 pip spreads and zero commission with no swap charges is not running a sustainable business model. Somewhere — usually in slippage, requotes, or the difference between mid-price and execution price — they are recovering the cost. Knowing where to look is the difference between a transparent broker and a problematic one.

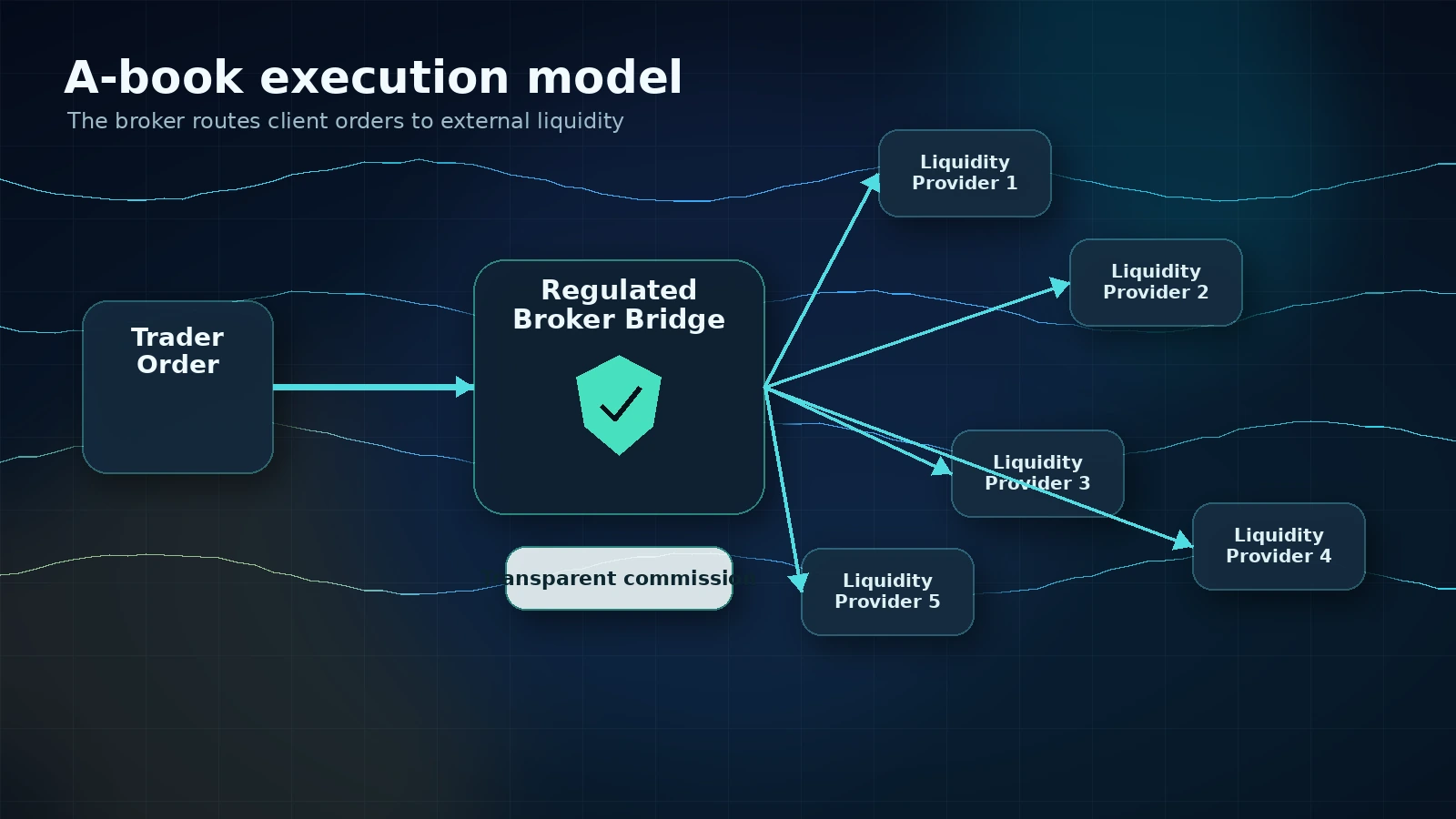

The A-Book Model — When the Broker Is Truly on Your Side

In an A-book or STP (straight-through processing) model, the broker passes your order through to one or more external liquidity providers — typically tier-1 banks, prime brokers, or non-bank market makers — and earns a commission on the volume. The broker does not take the opposite side of your trade. Whether you win or lose is, financially, none of their business.

This is the model traders generally want for one structural reason: the broker's interests are aligned with yours. They earn more when you trade more. They want you alive and active for as long as possible. A blown-up account is a churned customer, not a windfall.

Brokers that publicly identify as A-book or ECN — IC Markets, Fusion Markets, Pepperstone, and most of the Cyprus and Australia regulated ECN tier — typically run pure A-book on FX majors and minors. Some run A-book on majors and B-book on more exotic instruments where they cannot easily lay off risk.

The trade-off is cost structure. A-book brokers must pay their liquidity providers, so spreads are competitive but not free. You pay either a wider spread or a tight raw spread plus an explicit commission. There is no scenario in which an A-book broker can offer you sub-bank pricing — the bank is the source of the price.

The other thing worth understanding about A-book execution is that during news events, when liquidity providers widen their spreads, your broker has no choice but to widen too. This is not the broker gouging you; it is the underlying market repricing risk. A broker that does not widen during NFP or a central bank decision is almost certainly internalising the risk — which means B-book.

The B-Book Model — When Your Loss Is Their Profit

In a B-book or market maker model, the broker takes the other side of your trade. They quote you a price, you trade against them, and the net of all client positions sits on their book. If you lose, they gain — directly, not via commission.

B-book is legal in most regulated jurisdictions but it carries an inherent conflict of interest that regulators watch carefully. The FCA, ASIC, and CySEC all require B-book brokers to disclose execution conflicts and to manage them via internal risk policies. Whether those policies are actually followed varies.

B-book is not automatically bad. Statistically, the majority of retail forex traders lose money over a 12-month window — between 70% and 85% in most regulator-published win-rate data. A B-book broker who simply nets the losing flow against the winning flow earns the average client loss without ever needing to manipulate execution. That is a legitimate, regulated business model, and the broker has no incentive to mistreat any individual trader.

The problem starts when a broker selectively widens spreads for clients they expect to be profitable, slows execution on winning trades, or rejects/requotes orders that have moved against the broker's book. Signs your broker may be doing this include: spreads that widen substantially during news but tighten again only after you have closed, frequent requotes specifically on positions that are already in profit, execution latency that is fine on losing trades but slow on winning ones, and unusually favourable entry fills that subsequently reverse hard.

Many large retail brokers in fact run a hybrid model — they B-book the bottom 70% of clients (statistically losing) and A-book the profitable minority whose flow is too dangerous to internalise. From a trader's perspective this is fine if you are being A-booked, but you have no way to know which side of the line your account is on.

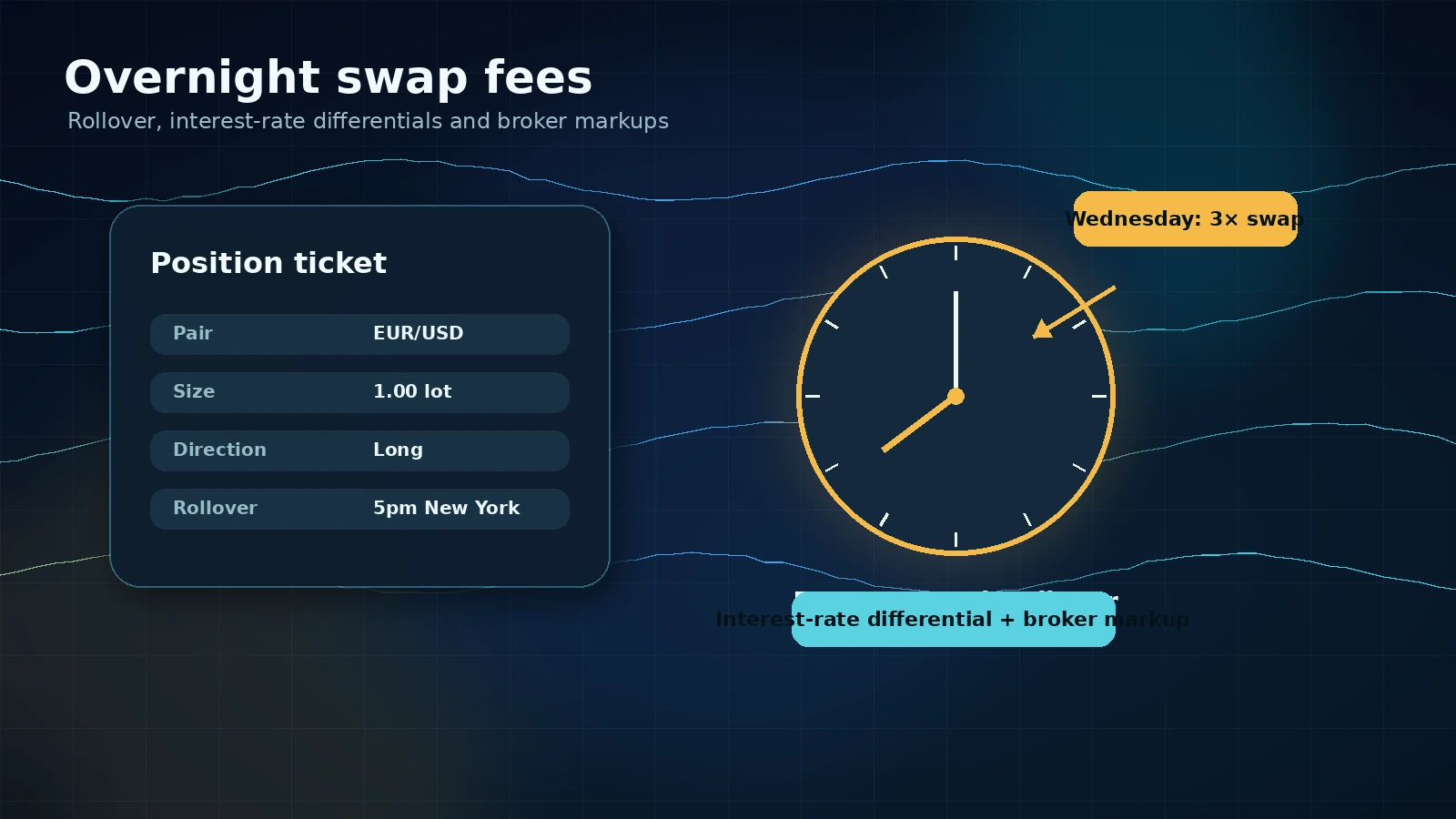

Overnight Swap Fees — The Hidden Revenue Stream

Swap fees are the line item retail traders most often ignore until they start running positions for more than a few days. Then they become the dominant cost.

When you hold a forex position past the daily rollover (5pm New York time), you either receive or pay the interest rate differential between the two currencies in the pair. The broker adds a markup on top of the underlying rate — typically equivalent to 0.5 to 1.5 percentage points annualised — and this markup is pure broker profit.

Wednesday rollover charges three days of swap to account for the weekend, since FX markets are closed Saturday and Sunday but settlement still rolls forward. A position held over a Wednesday close therefore costs (or earns) three times the daily swap. Traders are routinely caught out by this when entering a position late Wednesday evening.

A worked example. Hold one standard lot of EUR/USD short for 365 days at a daily swap credit of $1.20 (positive because of the current rate differential). Annual swap earned: roughly $438. Reverse it — one standard lot long, daily debit of -$3.40 (broker markup widens the differential against you). Annual swap paid: roughly $1,241. Same position, opposite direction, nearly $1,700 swing in carrying cost.

Islamic (swap-free) accounts are offered by most major brokers to comply with Sharia law's prohibition on interest. Brokers typically recover the cost in one of three ways: a flat administration fee after a holding period (often 5 days), slightly wider spreads on the swap-free account, or restrictions on which instruments are available. None of these are hidden in well-regulated brokers, but they vary widely.

| Pair (1 lot) | IC Markets | Fusion Markets | Vantage | eToro |

|---|---|---|---|---|

| EUR/USD long | -$8.40 | -$7.95 | -$9.20 | -$11.40 |

| USD/JPY long | +$5.10 | +$5.40 | +$4.60 | +$2.80 |

| GBP/USD short | -$3.20 | -$2.90 | -$3.80 | -$5.10 |

Indicative figures — swap rates change daily based on central bank rates. Always check current rates on your broker's contract specifications page before holding positions overnight.

How to Choose a Broker That's Not Working Against You

There is no single test that proves a broker is fully A-book, but there is a reliable checklist that filters out the worst-aligned brokers from your shortlist.

Look for explicit ECN/STP designation in the broker's account types. A genuine ECN account names its liquidity providers either in marketing material or in the product disclosure statement. A broker that cannot or will not say where its prices come from is almost always running an internal book.

Check for tight raw spreads plus commission rather than zero-commission wider spreads. Raw spread plus commission models are difficult to operate as pure B-book because the commission has to be passed somewhere — it is structurally an A-book signal.

Verify Tier-1 regulation: ASIC, FCA, or MAS. Tier-2 jurisdictions (CySEC, FSCA) are acceptable but offer less recourse if execution complaints arise. Offshore-only regulation (Vanuatu, St. Vincent, Mauritius) provides essentially no recourse and should be a last resort, not a first.

Test execution during news. Open a small position 30 seconds before a high-impact release and observe what happens at the print. Honest brokers widen their spreads to match liquidity provider quotes. Problematic brokers requote, freeze, or slip your fill far beyond what the underlying market shows on a third-party feed.

Check withdrawal speed history on third-party review aggregators (Trustpilot is noisy but readable in aggregate; ForexPeaceArmy is messier but useful for unresolved-complaint patterns). Slow withdrawals correlate strongly with hybrid B-book books that have run out of margin.

The brokers we most commonly recommend for transparent execution are IC Markets (visit) for raw spread plus commission ECN, Fusion Markets (visit) for the lowest cost structure available to retail, and Vantage (visit) for traders who also want copy trading. All three are Tier-1 regulated.

Risk warning. CFD trading involves significant risk and 74–89% of retail investor accounts lose money. Past execution quality is not a guarantee of future performance. This article is informational and does not constitute financial advice.

📖 Key Terms — Forex Glossary

Not sure about a term?Browse our full Forex Glossary →

Frequently Asked Questions

Expert Answers to Common Queries